Federal Solar Tax Credit 2026: How to Claim the 30% ITC (Step-by-Step Guide)

The federal solar tax credit is 30% in 2026, locked in through 2032 by the Inflation Reduction Act. It applies to panels, inverter, racking, wiring, permits, battery storage, and labor. You claim it on IRS Form 5695, transferring the credit to Schedule 3, Line 5 of Form 1040. It is non-refundable but carries forward indefinitely. You must own the system — leases don’t qualify. On a $20,000 system, that’s $6,000 directly off your federal tax bill.

The federal solar Investment Tax Credit lets US homeowners cut 30% directly off their federal tax bill when they install a qualifying solar system — and in 2026 that credit is fully intact at its maximum rate. For the average residential system costing around $28,000 before incentives, that works out to an $8,400 reduction in what you owe the IRS.

That’s not a deduction from your taxable income — it’s a dollar-for-dollar reduction of your actual tax bill. The difference is enormous. A $8,400 deduction might save you $2,000 in taxes depending on your bracket. A $8,400 credit saves you exactly $8,400.

This guide tells you exactly who qualifies, every cost that counts, how to file Form 5695 correctly, how the carry-forward works, and the six mistakes that cause homeowners to leave thousands on the table.

Part of the Shalkot DIY Solar Series

This is Article 10 — the financial capstone of our solar series. For system sizing see Article 01 — Solar Panel Calculator. For total system cost see Article 09 — DIY Solar Cost Breakdown. For installation see Article 02 — Complete Installation Guide.

What Is the Federal Solar Tax Credit?

The federal solar Investment Tax Credit (ITC) is a provision under Internal Revenue Code Section 25D — the Residential Clean Energy Credit — that allows US homeowners to claim 30% of their total qualified solar installation costs as a direct credit against their federal income tax liability.

In 2026, most homeowners who purchase and place in service a qualifying rooftop solar system and/or a battery of at least 3 kWh can claim a 30% nonrefundable federal income tax credit on eligible costs under the Residential Clean Energy Credit. That headline rate — extended by the Inflation Reduction Act — applies through 2032.

Tax Credit vs Tax Deduction — The Critical Difference

A tax deduction reduces your taxable income — a $8,000 deduction saves you $8,000 × your tax rate (typically 22–37% for middle-income households), or $1,760–$2,960.

A tax credit reduces your actual tax bill dollar-for-dollar — a $8,000 credit saves you exactly $8,000. The solar ITC is a credit. This is why it’s one of the most powerful financial incentives available to US homeowners.

Credit Rate Schedule: 2026 Through Expiration

The Inflation Reduction Act locked in the 30% rate through 2032 — then it steps down before expiring for residential systems. Here’s the full schedule:

Source: IRA 2022 (Pub. L. 117-169); IRS §25D; Form 5695 Instructions. The credit has been extended multiple times by Congress historically — the 2035 expiration may change. Plan based on current law, not speculation.

What “Placed in Service” Means for Your Credit Year

The credit applies to the tax year in which your system was fully installed and operational — meaning interconnected to the grid (or battery complete for off-grid). If your system was installed in December 2026, you claim it on your 2026 return filed in early 2027. A system that is purchased, contracted, or partially installed but not yet operational does not qualify yet — the clock starts at Permission to Operate (PTO) from your utility.

Who Qualifies — Eligibility Requirements

What Costs Qualify (and What Doesn’t)

Homeowners who rely on memory rather than their final itemized invoice routinely under-claim by $500 to $1,500 by forgetting permit fees, electrical panel upgrades, or monitoring system costs. Keep every invoice and receipt from the project, including items that seem incidental.

| Cost Item | Qualifies? | Notes |

|---|---|---|

| Solar panels / PV cells | ✅ Yes | All panel costs including shipping qualify |

| Inverter (string, micro, or hybrid) | ✅ Yes | Full cost of inverter including any accessories |

| Racking and mounting hardware | ✅ Yes | Rails, standoffs, flashing, clamps, all hardware |

| Electrical wiring and conduit | ✅ Yes | PV wire, MC4 connectors, EMT conduit, disconnects |

| Permit fees | ✅ Yes | City building permit, electrical permit, utility interconnection fees |

| Electrician labor | ✅ Yes | Any professional labor costs you pay qualify |

| Battery storage (3 kWh+ capacity) | ✅ Yes — 30% | LiFePO4 banks, Powerwall, EcoFlow batteries all qualify |

| Sales tax on equipment | ✅ Yes | Include all sales tax paid on qualifying equipment |

| Electrical panel upgrade | ✅ Yes (if required) | Only if the upgrade was directly necessitated by the solar installation |

| Monitoring system / equipment | ✅ Yes | Hardware cost of monitoring equipment qualifies; subscriptions do not |

| Your own unpaid labor | ❌ No | The IRS does not assign dollar value to your own installation time |

| Roof repairs / replacement | ❌ No | Unless the repair was specifically required to mount the solar system |

| Tree removal for shade clearing | ❌ No | Landscaping costs never qualify |

| Monitoring subscription fees | ❌ No | Ongoing service fees don’t qualify — one-time equipment cost does |

| Extended warranties / insurance | ❌ No | Protection plans and insurance premiums don’t qualify |

Free Solar Tax Credit Calculator

How to Claim: IRS Form 5695 Step-by-Step

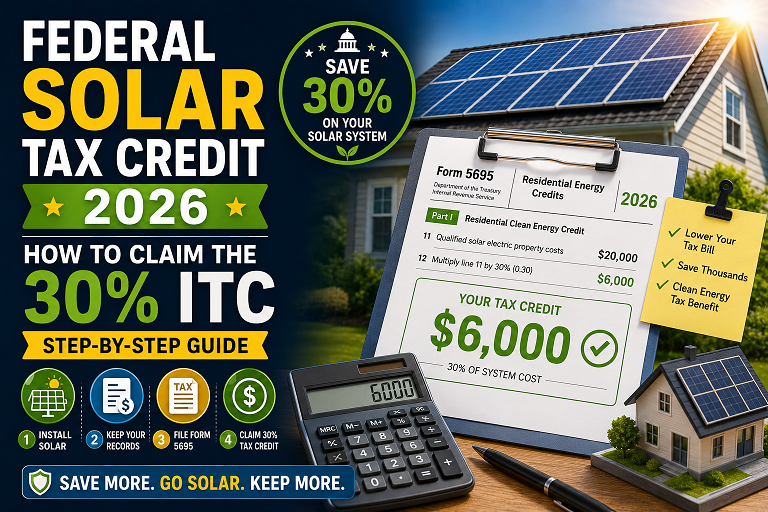

Claiming the solar ITC is straightforward. Complete IRS Form 5695 (Residential Energy Credits) with your federal tax return. Enter your total eligible system cost, calculate 30%, and transfer the result to Schedule 3, Line 5 of your Form 1040. All major tax software guides you through this automatically.

Here is the exact process, step by step:

Gather Your Documentation

Collect every invoice, receipt, and payment record from your solar project: final equipment invoice from your supplier, permit fee receipts, electrician invoice, sales tax records, and your utility’s Permission to Operate (PTO) letter. The PTO letter establishes the “placed in service” date — the date that determines which tax year you claim the credit.

Calculate Your Total Qualified Expenses

Add up all qualifying costs from the table above. Use the calculator in this article or simply total every invoice for equipment, labor, permits, and battery storage. Subtract any rebates or subsidies first, then enter the result on IRS Form 5695 Line 1. State rebates you received reduce your qualifying basis; federal grants would too (but there are currently no federal solar grants for residential systems in 2026).

Form 5695, Part I, Line 1 — Total qualified solar electric property costsComplete IRS Form 5695, Part I

Part I is for the solar credit. Enter your total qualified solar expenses on Line 1. Calculate your credit — multiply your total qualified expenses by 0.30 (30%). Enter this on Line 6b of Form 5695. Part I covers Lines 1–14 and walks you through combining any other residential energy credits (geothermal, wind, fuel cells) with your solar credit for a total residential clean energy credit amount.

Line 1 → Your total costs Line 6b → Multiply Line 1 × 0.30Transfer to Schedule 3 and Form 1040

Transfer to Form 1040 — the credit amount flows from Form 5695 to Schedule 3 (Form 1040), Line 5. This directly reduces your tax liability. Schedule 3 totals all non-refundable credits and feeds them into your Form 1040, Line 20 (Other Credits). Your total tax due is reduced by the credit amount. If the credit exceeds your tax liability, the remainder carries forward (see Section 7).

Form 5695 → Schedule 3, Line 5 → Form 1040, Line 20File Your Return

Include Form 5695 and Schedule 3 with your federal tax return for the year your system was placed in service. Electronic filing (e-file) processes Form 5695 credits in 6–8 weeks. Paper filing takes 12–16 weeks. E-filing is strongly recommended for faster processing and fewer errors. You do not mail in your receipts or PTO letter — keep them for your records in case of audit.

Non-Refundable Credit and Carry-Forward Rules

This is the section most homeowners get wrong — and misunderstanding it causes real financial mistakes.

The 30% solar tax credit is non-refundable. This means: if your total tax liability for 2026 is $8,000 and your solar credit is $12,000, you’ll only get $8,000 off your taxes that year. The remaining $4,000 doesn’t disappear — it carries forward to future tax years.

What If You Have Very Low or Zero Federal Tax Liability?

Homeowners who are retired and live primarily on Social Security income, or who have very low taxable income for other reasons, may find they cannot fully use the credit within a reasonable timeframe. In those cases, the financial case for solar still exists, but it is weaker than for households with substantial ongoing federal tax liability.

Specifically: Social Security income is often partially or fully excluded from federal taxation. If you owe $0 in federal taxes each year, the carry-forward never gets consumed and you receive no financial benefit from the credit. If this applies to you, consult a tax professional before making the solar purchase decision — the economics change significantly without the credit benefit.

Battery Storage Credit — Updated Rules for 2026

The Inflation Reduction Act made a significant change to battery storage eligibility starting in 2023 that many homeowners still don’t know about:

| Battery Storage Scenario | Qualifies? | Credit Rate | Notes |

|---|---|---|---|

| Battery installed with solar system simultaneously | ✅ Yes | 30% | The most common scenario — battery cost adds to total qualified basis |

| Battery added to existing solar system later | ✅ Yes | 30% | Can claim credit on battery cost in the year it is installed, even years after panels |

| Standalone battery (no solar panels at all) | ✅ Yes (since 2023) | 30% | New under IRA — a battery alone without solar now qualifies at full 30% |

| Battery under 3 kWh capacity | ❌ No | — | Minimum 3 kWh required — most home batteries (10–20 kWh) easily exceed this |

| Battery in a leased solar system | ❌ No | — | Must own the battery — the installer claims the credit on leased equipment |

The Battery Tax Credit Is a Genuine 2026 Opportunity

Starting in 2023, standalone residential battery storage technology of at least 3 kWh capacity qualifies at 30% — no requirement that the battery be charged only from solar. This means if you install a 10 kWh LiFePO4 battery bank costing $2,500, you receive a $750 federal tax credit on that purchase alone. If you already have solar panels and want to add battery backup in 2026, you can claim the 30% credit on the battery cost in your 2026 tax return separately from your original solar credit. For battery sizing help, see our Battery Bank Calculator.

Stacking State Incentives on Top of the Federal Credit

Top state programs add thousands more: NY, MA, NJ, MD, CA, CO lead. The federal 30% ITC is just the floor — many states offer additional credits, rebates, and tax exemptions that stack directly on top of it, making the total incentive picture even more favorable.

Find Every Incentive in Your Zip Code

The Database of State Incentives for Renewables and Efficiency (DSIRE) at dsireusa.org lists every active solar incentive in every US state and many local utilities. Enter your zip code to see every program currently available. This takes 10 minutes and is worth doing before you buy — some local utility programs and HOA incentives are not widely advertised but can add $500–$3,000 to your savings.

6 Mistakes That Cost Homeowners Money on the Solar Tax Credit

The credit applies to the year your system was placed in service — not the year you signed a contract, paid a deposit, or even finished physical installation. “Placed in service” means your utility issued Permission to Operate (PTO). If PTO arrived January 3, 2027, you claim the credit on your 2027 return — not 2026. Keep your PTO letter and use its date as your reference point.

Homeowners routinely under-claim by $500 to $1,500 by forgetting permit fees, electrical panel upgrades, or monitoring system costs. Every dollar you forget to include in your qualified basis costs you 30 cents in lost credit. Total every receipt — panels, inverter, racking, wiring, conduit, MC4 connectors, permits, electrician invoices, and sales tax on all equipment.

Claiming the credit in a year where your tax liability is zero — without understanding the carryforward mechanism — leads some homeowners to believe they lost the credit entirely. They have not. Unused credit carries forward indefinitely to future tax years. You never lose it. However, if you have zero federal tax liability every year for the foreseeable future (common for retirees living on Social Security), the carryforward may never be consumed — factor this into your decision.

Homeowners who lease solar panels or sign a PPA are not the system owner — the installer is. The installer claims the ITC, not you. This is one of the primary reasons purchasing solar (including with a solar loan) is financially superior to leasing in 2026. With a solar loan, you own the system from day one, claim the full 30% credit on the total installed cost (not just your down payment), and can use the credit to make a lump-sum loan payment in year one.

If your solar installation required a main electrical panel upgrade (common in homes with 100A panels or full breaker boxes), that cost qualifies for the 30% credit — but only if the upgrade was directly necessitated by the solar installation. Document this in writing: get your electrician to note on the invoice that the panel upgrade was required for the solar interconnection. This $1,200–$2,500 cost at 30% credit = $360–$750 you could be missing.

The federal credit and state credits are completely independent and can be stacked. A New York homeowner can claim the 30% federal ITC plus New York’s 25% state credit (up to $5,000) on the same installation — potentially receiving credits totaling 45–55% of system cost. Check DSIRE.org before installing — missing a state incentive because you didn’t know it existed is an entirely avoidable loss.

Calculate Your Full System Cost Including Tax Credit

Use our DIY Solar Cost guide to build your complete budget — then apply the 30% credit calculator above to see your exact net cost and payback period.

Frequently Asked Questions

What is the federal solar tax credit percentage in 2026?

In 2026, most homeowners who purchase and place in service a qualifying rooftop solar system can claim a 30% nonrefundable federal income tax credit on eligible costs. That headline rate — extended by the Inflation Reduction Act — applies through 2032. After 2032, the credit steps down to 26% in 2033, 22% in 2034, and expires for residential systems in 2035 unless Congress extends it again.

Does the 30% solar tax credit apply to DIY solar installations?

Yes, fully. The IRS does not require a licensed installer to claim the residential solar tax credit — it requires that you own the system and that it is placed in service at your US residence. For DIY installations, all equipment costs (panels, inverter, racking, wiring, battery storage), permit fees, and any professional labor you pay to others qualify. Your own unpaid installation time does not qualify, but everything you pay others for does.

What costs qualify for the federal solar tax credit?

Qualifying costs include: solar panels, inverter, racking and mounting hardware, electrical wiring and conduit, disconnects, permit fees, battery storage of at least 3 kWh, sales tax on all qualifying equipment, labor costs paid to electricians or installers, and electrical panel upgrades directly required by the solar installation. Costs that do not qualify include your own unpaid labor, roof repairs unrelated to solar mounting, landscaping, and ongoing monitoring subscriptions.

What if I don’t owe enough taxes to use the full solar credit?

The remaining credit doesn’t disappear — it carries forward to future tax years. Any unused portion of the 30% solar tax credit carries forward indefinitely to subsequent tax returns until fully consumed. If your credit is $7,500 but you only owe $4,000 this year, $4,000 is applied now and $3,500 carries to next year automatically via Form 5695’s carryforward line. There is no expiration on unused carryforward amounts.

Does the solar tax credit apply to battery storage in 2026?

Starting in 2023, standalone residential battery storage technology of at least 3 kWh capacity qualifies at 30% — no requirement that the battery be charged only from solar. This means adding a LiFePO4 battery bank to your solar system, or installing a standalone battery for backup power without any solar panels, both qualify for the full 30% credit in 2026. The battery must be installed at your US primary or secondary residence and you must own it.

Can I claim the solar tax credit if I lease my panels?

No. You must own your solar system to claim the federal tax credit. When you lease panels or sign a power purchase agreement (PPA), the installer retains ownership and claims the ITC — not you. This is one of the primary financial reasons to purchase solar outright or with a solar loan rather than leasing. With a solar loan, you own the system from day one and can claim the full 30% credit on the total installed cost, not just your down payment.

How do I claim the federal solar tax credit?

Complete IRS Form 5695 (Residential Energy Credits) with your federal tax return. Enter your total qualified solar expenses on Line 1. Calculate your credit by multiplying by 0.30 and enter on Line 6b. Transfer to Form 1040 — the credit flows from Form 5695 to Schedule 3, Line 5, directly reducing your tax liability. File Form 5695 with your federal tax return for the year your system was placed in service. All major tax software (TurboTax, H&R Block, TaxAct) handles Form 5695 automatically.

Complete Your Solar Financial Picture

- SolarProGuide — Federal Solar Tax Credit 2026: Complete Guide to the 30% ITC, March 2026

- HomeCostLab — Solar Tax Credit 2026: How to Claim the 30% Federal ITC, April 2026

- DigitalWindmill — Federal Solar Tax Credit 2026: 30% Rules and How to Claim, June 2026

- GreenEnergyCalc — Federal Solar Tax Credit 2026: The Complete Guide, April 2026

- SolarPowerSimplified — How to Claim 30% Federal Solar Tax Credit 2026 IRS Form 5695 Guide, February 2026

- TrySolar.Pro — Solar Tax Credits 2026: ITC, Rebates and How to Claim, March 2026

- Boston Solar — How to Claim Federal Solar Tax Credit: 6-Step Guide 2026, April 2026

- IRS — Form 5695, Residential Energy Credits (2025 tax year, filed 2026)

- IRS — Schedule 3 (Form 1040), Additional Credits and Payments

- Inflation Reduction Act (Pub. L. 117-169) — IRC §25D extension through 2032

- DSIRE — Database of State Incentives for Renewables and Efficiency, dsireusa.org

- SEIA — Solar Investment Tax Credit (ITC) Fact Sheet, 2026

3 thoughts on “Federal Solar Tax Credit 2026: How to Claim the 30% ITC (Step-by-Step)”